Buying health insurance isn’t just a financial decision—it’s a long-term safety net for you and your family. Yet, many people rush into buying a policy without understanding key details, which often leads to claim issues or insufficient coverage later.

This

health insurance checklist will help you make a smart, informed decision before you commit.

Why You Need a Checklist Before Buying Health Insurance

Health insurance policies can be complex. Without proper evaluation, you might:

- Choose insufficient coverage

- Miss hidden conditions or exclusions

- Pay higher premiums for fewer benefits

- Face claim rejections

A structured checklist ensures you don’t overlook critical details.

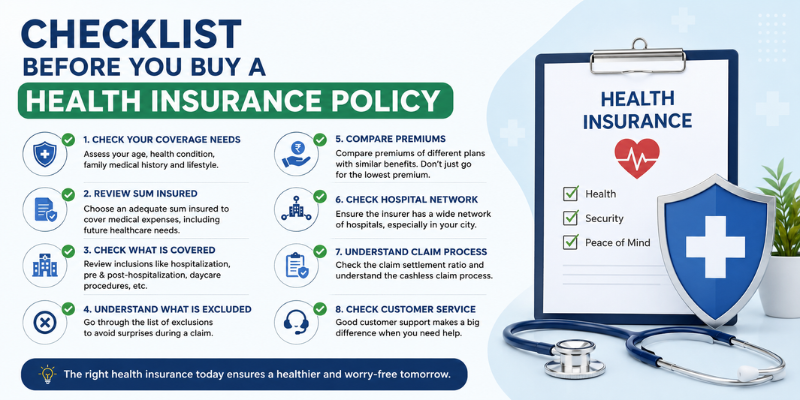

✅ Complete Checklist Before Buying Health Insurance

1. Assess Your Coverage Needs

Start by understanding how much coverage you actually need.

- Individual: ₹10–15 Lakhs

- Family: ₹15–25 Lakhs

- Metro cities: ₹25 Lakhs+

Consider factors like age, lifestyle, city, and medical history.

👉 Tip: Don’t just go for the cheapest plan—focus on adequate coverage.

2. Compare Multiple Plans

Never buy the first plan you see.

- Compare premiums vs benefits

- Check hospital network

- Analyze coverage inclusions

👉 Use a smart

Policy Analyser to compare multiple policies side by side and identify the best fit.

3. Check What’s Covered (Inclusions)

Carefully review what the policy includes:

- Hospitalization expenses

- Pre & post hospitalization

- Daycare procedures

- Critical illness coverage

Make sure major treatments are covered.

4. Understand What’s NOT Covered (Exclusions)

This is where most people make mistakes.

Common exclusions include:

- Pre-existing diseases (initial waiting period)

- Cosmetic procedures

- Self-inflicted injuries

- Alternative treatments (in some plans)

👉 Always read the fine print before purchasing.

5. Look at Waiting Periods

Every policy has waiting periods for certain conditions:

- Pre-existing diseases: 2–4 years

- Specific illnesses: 1–2 years

- Maternity benefits: 2–4 years

Shorter waiting periods are always better.

6. Check the Claim Settlement Ratio

This tells you how reliable the insurer is.

- Higher ratio = better chances of claim approval

- Look for insurers with consistent performance

7. Network Hospitals & Cashless Facility

Ensure the insurer has a wide hospital network.

- Cashless treatment reduces out-of-pocket expenses

- Check hospitals near your location

8. No Claim Bonus (NCB)

A good policy rewards you for staying healthy.

- Increases your sum insured every claim-free year

- Helps you build higher coverage without extra cost

9. Sub-limits and Co-payment

Watch out for hidden cost-sharing clauses:

- Room rent limits

- Disease-specific caps

- Co-payment requirements

These can significantly increase your out-of-pocket expenses.

10. Premium vs Benefits (Value for Money)

Don’t choose a policy just because it’s cheap.

Ask yourself:

- Does it offer adequate coverage?

- Are the benefits worth the premium?

👉 Balance affordability with comprehensive coverage.

11. Lifetime Renewability

Always choose a policy that offers lifetime renewability.

- Ensures coverage even in old age

- Avoids future policy switching issues

12. Add-ons and Riders

Enhance your policy with add-ons like:

- Critical illness cover

- Maternity cover

- Room rent waiver

- OPD cover

Choose only what you actually need.

13. Easy Policy Management

A good platform should allow you to:

- Compare plans easily

- Understand policy details clearly

- Get expert recommendations

👉 Platforms like

Staywell Health simplify this process by offering easy comparison and guidance in one place.

🚫 Common Mistakes to Avoid

- Buying insurance too late

- Ignoring policy exclusions

- Choosing low coverage to save premium

- Not comparing multiple plans

- Skipping the fine print

📊 Pro Tip: Think Long-Term

Health insurance isn’t just for today—it’s for the future.

With rising healthcare costs, your policy should:

- Adapt to medical inflation

- Cover major illnesses

- Provide long-term financial protection

Final Thoughts

Buying health insurance without proper research can lead to costly mistakes. This checklist ensures you choose a policy that truly protects you when you need it most.

Take your time, compare wisely, and focus on long-term benefits—not just short-term savings.

✅ Take the Next Step

✔️ Evaluate your needs

✔️ Compare plans carefully

✔️ Choose smart coverage

👉 Ready to secure your future?

Buy Health Insurance Now and make a confident decision.

By:

By: